Sydney Prefab Backyard Homes Market Research Report V2.0

Based on authoritative sources such as ABS trade data, NCC building codes, and HIA industry surveys, this analysis comprehensively examines the pre-fabricated granny flat market on the cusp of explosion and its breakthrough paths from eight dimensions: supply-side (AUD $278.5 million import value from Chinese factory capacity), demand-side (262,000 housing shortfall), regulatory-side (WaterMark/CodeMark/NATA certification barriers), design blind spots (wind loads/7-star energy efficiency), and the practical constraints of backyard construction in Sydney.

Executive Summary

This report provides a comprehensive and in-depth analysis of the Sydney and Australian prefabricated granny flat/secondary dwelling market. Based on public data from authoritative bodies such as the Australian Bureau of Statistics (ABS), NSW Planning, Housing Industry Association (HIA), and Australian Building Codes Board (ABCB), combined with industry-leading research and the latest trade statistics, the report conducts an in-depth analysis across eight dimensions: supply side (Chinese factory capacity and exports), demand side (housing shortage and immigration growth), regulatory side (building standards and certification systems), financial side (lending environment), market structure (granny flats vs. House & Land Packages), deep compliance certification barriers, design blind spots, and practical constraints of backyard construction in Sydney.

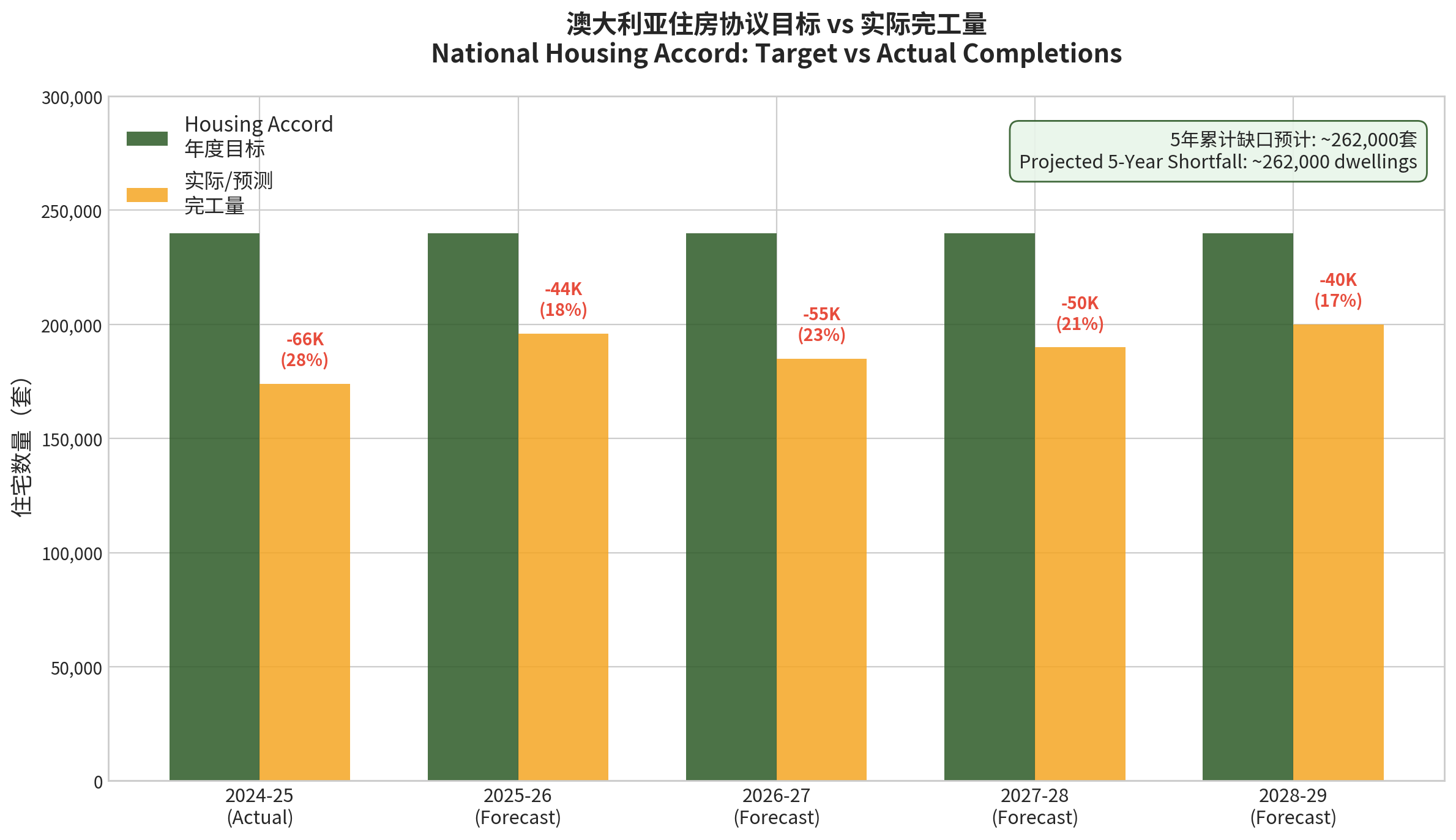

Key findings are as follows: Australia faces a five-year housing deficit of approximately 262,000 dwellings (Housing Accord targets vs. actual completions), and granny flats, as a "no new land required" housing solution, are benefiting from both policy and market tailwinds. HIA surveys indicate that builders expect to construct 10 times the number of granny flats in 2026 compared to 2022 [1]. Concurrently, by the 2024-25 financial year, Australia's prefabricated building imports reached a record A$278.5 million, with China accounting for 67.8% of the market share [2]. However, due to the strict and unique nature of Australian building standards (NCC/BCA)—particularly the mandatory WaterMark plumbing certification, CodeMark building system certification, and NATA steel traceability reports, which represent systemic certification barriers—over 99% of Chinese factory products cannot directly meet Australian compliance requirements [3]. The core bottleneck lies not only in the lack of "active design" involvement from local Australian architectural and structural firms but also in a fundamental lack of understanding of Australia's "systemic certification" logic.

The report further points out that the true breakthrough path for the Sydney granny flat market is not "large modular complete units" but a lightweight modular system based on systematic deconstruction design, calibrated by local construction experience, and constrained by lateral transport and backyard access. A hybrid model of "90% offshore production + 10% local fabrication (foundations, connections, installation)" is the optimal path to address Australia's housing challenges, but its widespread adoption requires simultaneously meeting four conditions: full-process design involvement from local firms, sufficient market demand, strong sales channels, and viable financing solutions.

1. Research Background and Methodology

1.1 Research Background

Over the past two years, the global geopolitical landscape has undergone profound changes, with escalating conflicts in the Middle East, intensifying Sino-US trade tensions, and the exposed fragility of global supply chains. Concurrently, Australia is facing its most severe housing crisis since World War II—the federal government's National Housing Accord set an ambitious target of building 1.2 million new homes within five years, but actual completions are significantly behind schedule. Against this backdrop, prefabricated construction, as a method that can significantly shorten construction times, reduce costs, and improve quality, is receiving unprecedented attention.

Sydney, as Australia's most populous city, faces particularly acute housing pressure. Granny flats (Secondary Dwellings), with their unique advantage of "not requiring new land, utilising existing backyard space," are seen as one of the key solutions to alleviate the housing crisis. The New South Wales government has simplified the approval process through "Complying Development Certificates" (CDC), allowing granny flat construction to be approved in as little as two weeks, with occupancy possible just 3-4 months from order placement.

However, the supply side of the market faces severe challenges. Numerous Chinese prefabricated housing factories, facing overcapacity due to the downturn in the domestic real estate market, have turned their attention to the Australian market, but the vast majority of their products fail to meet Australia's stringent building standards. This supply-demand mismatch forms the core research problem of this report.

1.2 Research Methodology

This report employs the following research methods:

| Method | Description | Data Sources |

|---|---|---|

| Desktop Research | Systematic collection and analysis of public data and reports | ABS, NSW Planning, HIA, ABCB, RBA |

| Industry Report Analysis | Citing data from authoritative market research institutions | Mordor Intelligence, Dallas Fed, McKinsey |

| Trade Data Analysis | Precise data on Australian prefabricated building imports and origin countries | ABS Trade Data, Industry Statistics |

| Policy Document Analysis | Reviewing federal and state housing and building policies | NCC 2022/2025, NSW SEPP, Housing Accord |

| Certification System Research | In-depth analysis of WaterMark/CodeMark/NATA systems | ABCB, Standards Australia, NATA |

| Media & Academic Literature | Cross-validation of key data points | SCMP, ArchiEng, ASCE, Nature |

| Frontline Industry Insights | Based on EASOVA team's practical market experience | Project operational data |

2. Chinese Prefabricated Housing Factory Overcapacity and Export to Australia

2.1 Current State of China's Prefabricated Construction Market

China's prefabricated construction market has experienced explosive growth over the past decade. According to industry data, the market size for prefabricated construction in China is expected to reach CNY 1.62 trillion in 2025, representing a year-on-year growth of 10.0% [4]. Research by Mordor Intelligence indicates that the Chinese prefabricated construction market was valued at approximately USD 69.74 billion in 2026 and is projected to grow at a compound annual growth rate of 6.99% to USD 97.86 billion by 2031 [5].

However, this growth conceals serious structural issues. Since the downturn in China's real estate market began in 2021, a large number of construction-related factories have faced significant reductions in orders and idle capacity. A research report by the Federal Reserve Bank of Dallas in December 2025 explicitly stated:

"China's manufacturing overcapacity problem began with the boom and bust cycle of its real estate sector. As domestic demand shrinks, excess capacity is being shifted to global markets through export channels." [6]

The steel structure prefabricated building sector is particularly prominent. China is the world's largest steel producer, with approximately 98% of global crude steel production in 2024 coming from 71 major steel-producing countries, and China holding an absolute dominant position [7]. After the domestic market contracted, steel structure factories increasingly sought overseas export markets, with prefabricated housing becoming an important channel for absorbing excess capacity.

2.2 Australia: A Core Destination for Chinese Prefabricated Housing Exports

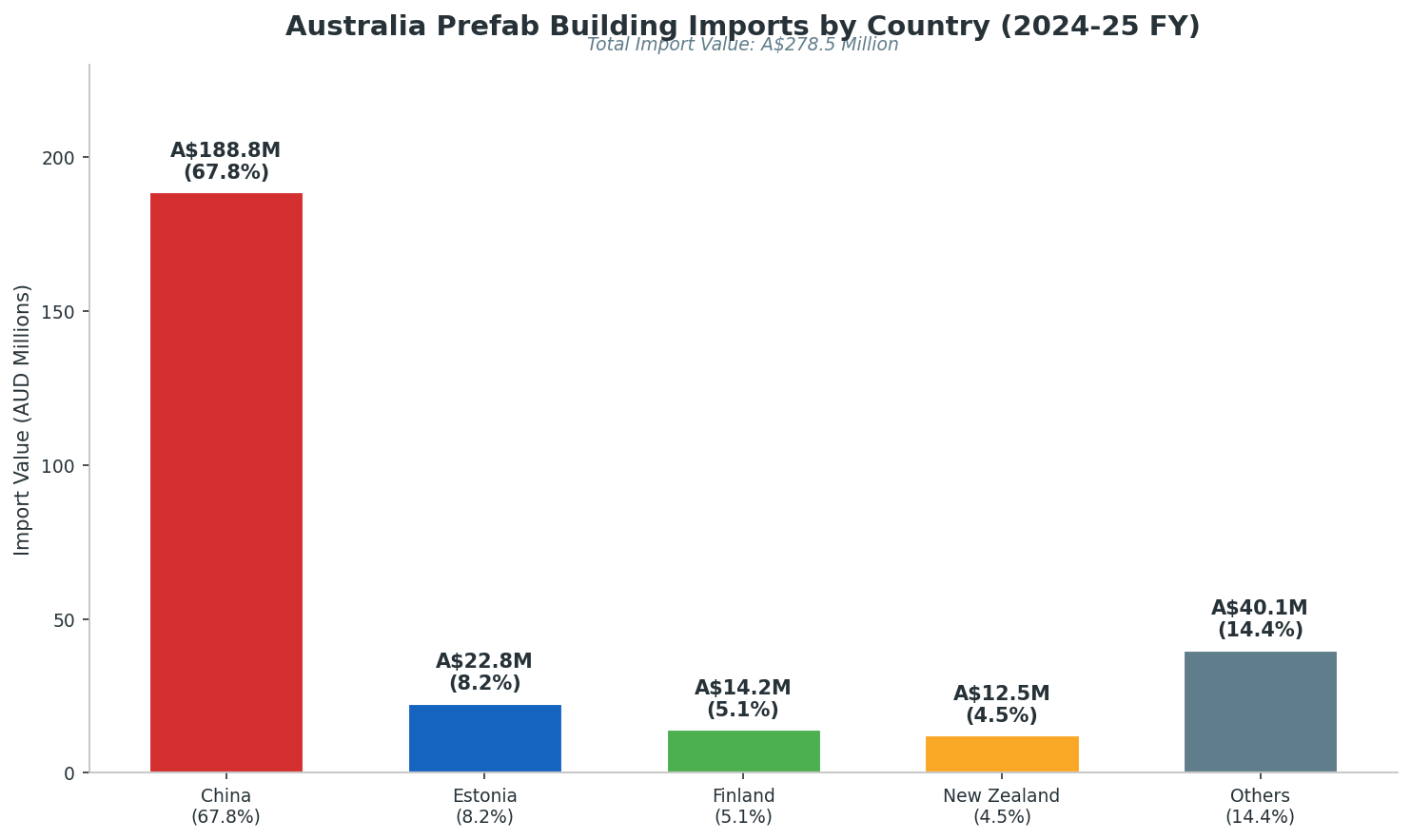

Data confirms that Chinese capacity is strongly spilling over into Australia. By the 2024-25 financial year, Australia's prefabricated building imports reached a record A$278.5 million. China is Australia's largest supplier of prefabricated housing, accounting for 67.8% of the total import market share [2]. In terms of material classification, China holds the strongest advantage in non-timber (e.g., steel structure, composite panel) prefabricated housing; in the high-precision timber prefabricated components market, China's share is approximately 43%, facing competition from European countries such as Estonia and Finland.

A report by Dracon NZ in April 2025 further noted that Australia is "strategically shifting towards Chinese modular housing" to address the multiple challenges facing its domestic construction industry—including skilled labour shortages, rising material costs, and extended construction times [8].

| Indicator | Data |

|---|---|

| Total Australian Prefabricated Building Imports (2024-25 FY) | A$278.5 million |

| China's Share of Australian Prefabricated Imports | 67.8% |

| China Prefabricated Construction Market Size (2025) | CNY 1.62 trillion (~USD 222B) |

| China Prefabricated Construction Market Size (2026) | USD 69.74 billion |

| China Prefabricated Market Annual Growth Rate | 10.0% (2025) |

| Estimated 2031 Market Size | USD 97.86 billion |

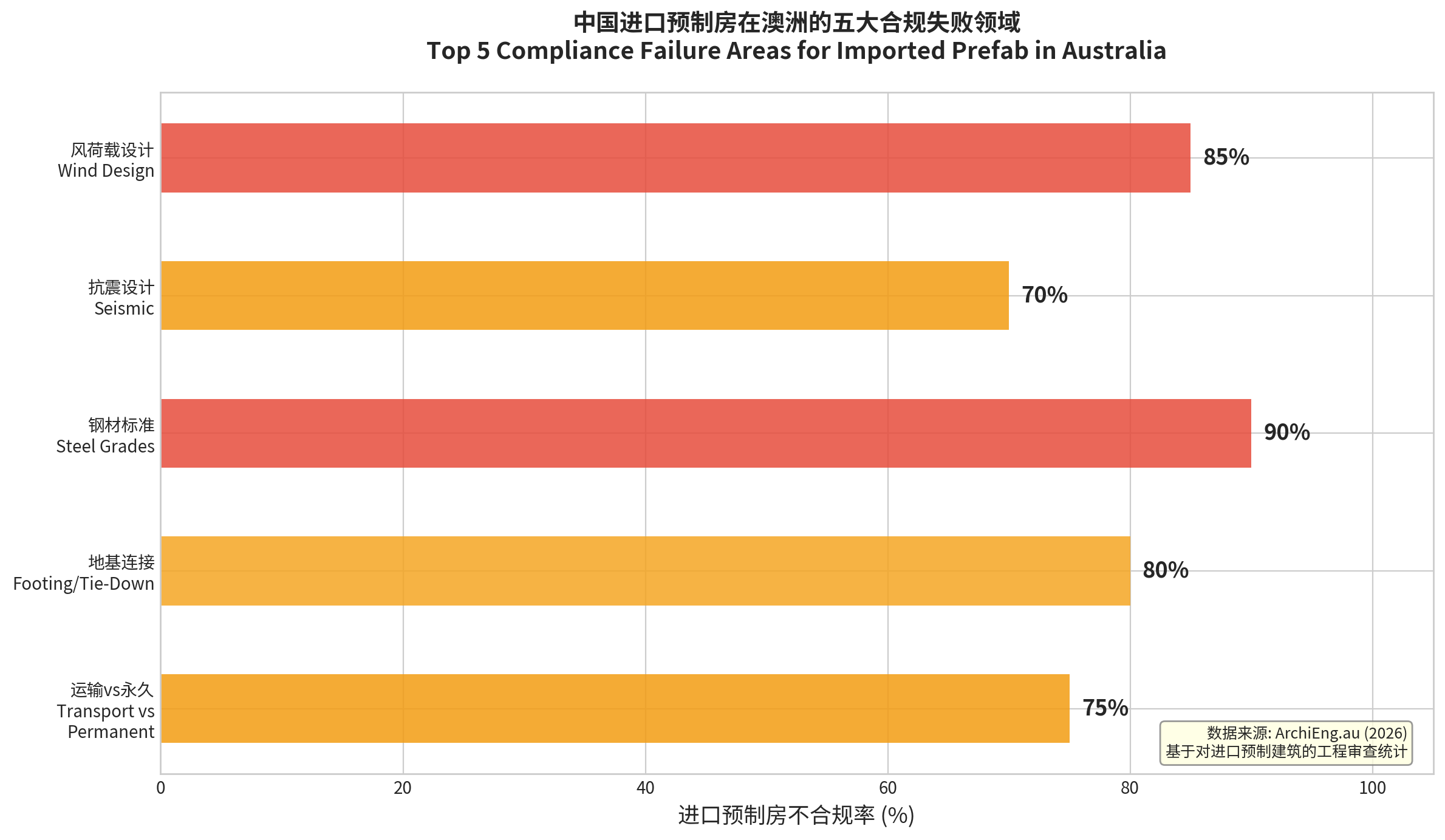

2.3 Why 99% of Chinese Factories Cannot Comply

Despite the clear advantages of Chinese factories in terms of capacity, price, and delivery speed, the vast majority of their products cannot directly meet Australian building standard requirements. An in-depth analysis published by ArchiEng in January 2026 stated:

"Many overseas manufacturers produce to very high standards, but these standards almost never align with Australia's unique National Construction Code (NCC)." [3]

The root cause of this problem is that Chinese factories generally fail to recognise their correct positioning within the Australian construction industry value chain. They attempt to enter the market with an "finished product export" model, rather than integrating as a "controlled manufacturing segment" within a design-manufacture-install system led by local Australian architectural and structural firms. Essentially, most overseas factories are not exporting a complete, ready-to-use "house" to Australia, but rather a "component system" or "semi-finished product system" with manufacturing capabilities. In Australia, for this system to become a truly deliverable residential product, it must first be re-integrated through local architectural design, structural design, construction logic, certification logic, and practical installation experience.

3. Australian Building Standard Compliance Barriers

3.1 National Construction Code (NCC) System

Australia's building standards system is centred around the National Construction Code (NCC), which is developed and maintained by the Australian Building Codes Board (ABCB). The preview version of NCC 2025 was officially released on February 1, 2026, introducing more explicit and stringent requirements for prefabricated buildings [9].

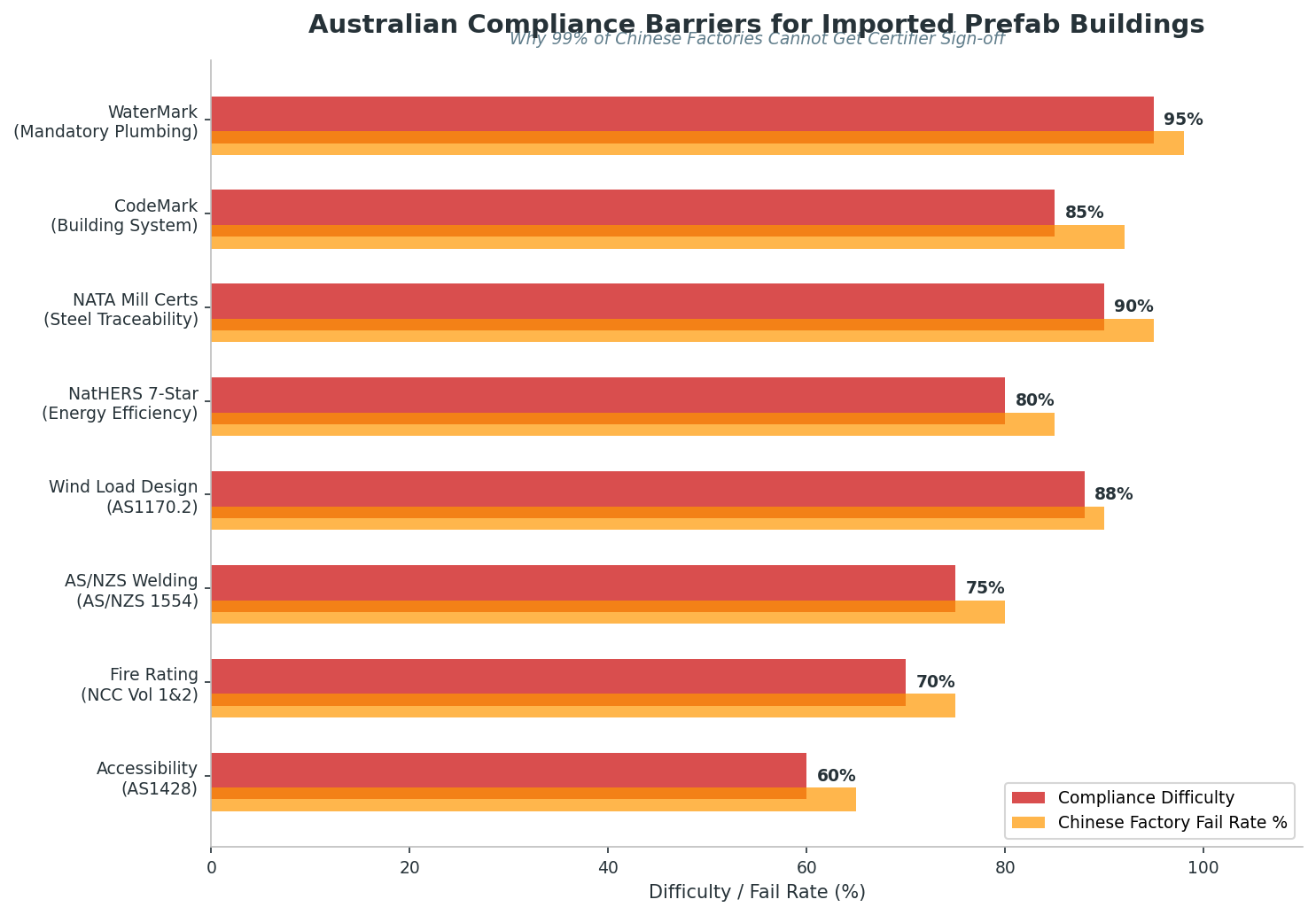

The NCC covers the following key areas, each of which is a mandatory requirement that imported prefabricated homes must meet:

| Compliance Area | Key Standard | Common Issues for Chinese Factories |

|---|---|---|

| Structural Integrity | AS1170 (Loads), AS4600 (Cold-formed Steel) | Insufficient wind load design (China ~100km/h vs. Australia 120-250km/h+) |

| Earthquake Design | AS1170.4:2024 | Even low-rise buildings must consider, generally overlooked by Chinese factories |

| Steel Standards | AS/NZS 1554 (Welding), AS4100 | Use of Q235/Q345 steel without NATA-approved mill test data |

| Foundation Connections | AS2870 (Residential Footings) | Inability to provide tie-down connection designs compliant with Australian standards |

| Fire Safety | NCC Volume 1 & 2 | Fire ratings, material flame retardancy not up to standard |

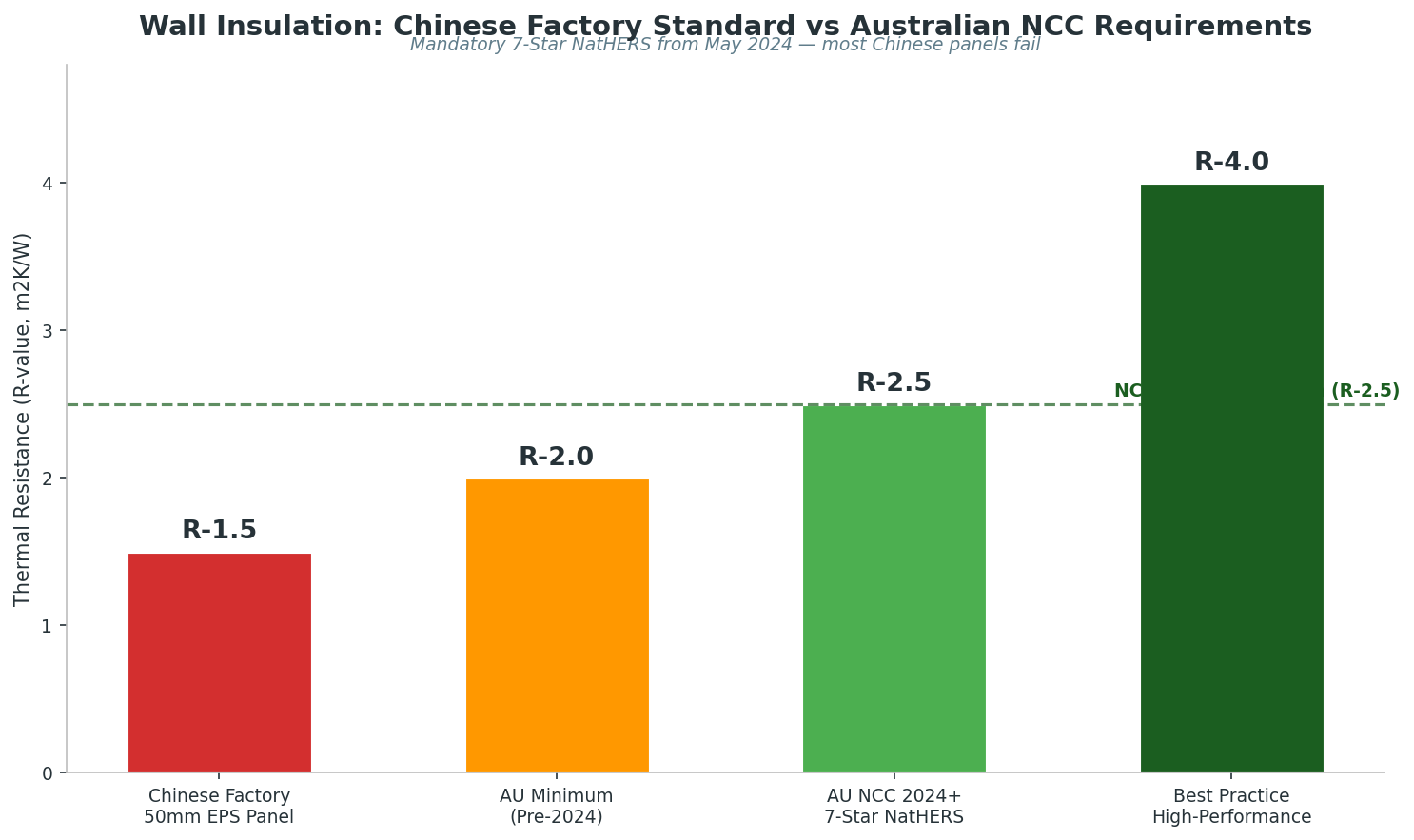

| Energy Efficiency | NCC Section J / NatHERS 7-star | 50mm EPS sandwich panels typically only R-1.5, far below R-2.5 requirement |

| Plumbing Certification | WaterMark (Mandatory) | Pre-installed taps/pipes/valves lack WaterMark logo |

| Accessibility Design | AS1428 | Non-compliant door widths, ramps, bathroom dimensions |

3.2 The Critical Role of Certifier Sign-off

In Australia's building approval system, the Certifier (Building Certifier / Private Certifier) plays a crucial role. Every critical construction stage requires sign-off from a certifier, including but not limited to: Construction Certificates during the design approval phase, Mandatory Inspections during construction, and Occupation Certificates upon completion.

Australian certifiers do not look at "how big the factory is" or "ISO certification," but rather at specific Product Certification. The personal professional liability of certifiers makes them extremely cautious about signing off on unfamiliar overseas design schemes. This means that even if a Chinese factory's product quality is excellent, if the design documentation is not "actively designed" by an Australian registered architect and structural engineer according to Australian standards, it is almost impossible for a certifier to sign off. The current market breakthrough is stalled at the interface between "Australian structural engineer sign-off (Reg 126 or Form 15)" and "transparency of factory manufacturing processes" [10].

3.3 ABCB's Direction for Reform

It is noteworthy that the ABCB has recognised the existing regulatory framework's impediment to prefabricated construction and, in July 2025, released an issues paper for a "National Voluntary Certification Scheme for Manufacturers of Modern Methods of Construction" [11]. This scheme aims to establish a nationally consistent certification framework, enabling prefabricated building manufacturers to demonstrate compliance with NCC requirements through third-party certification, thereby simplifying state-level approval processes.

The HIA, in its submission, stated:

"For prefabricated construction, third-party certification is needed to confirm that the building's design drawings and specifications comply with NCC requirements." [12]

While this direction for reform is positive, it will still take time to implement. Market participants currently still need to rely on the traditional "local design + certifier sign-off" path.

4. Deep Compliance Certification Barriers: WaterMark, CodeMark, and NATA

This chapter delves into the three major systemic certification barriers that Chinese prefabricated homes face in Australia. These barriers are not simply "different standards" but stem from a fundamental lack of understanding of Australia's "systemic certification" logic.

4.1 WaterMark: The Biggest "Trap" for Chinese Prefabricated Homes

WaterMark is Australia's mandatory plumbing product certification system. According to Australia's Water Efficiency Labelling and Standards Act, all plumbing products installed in Australia—including taps, pipes, valves, showers, toilets, etc.—must bear the WaterMark certification mark.

This poses the most direct compliance obstacle for Chinese prefabricated homes. If pre-installed taps, pipes, and valves inside the module lack the WaterMark logo, Australian licensed plumbers cannot legally connect and install them and may even have their licenses revoked. This means that even if the entire prefabricated home's structure, insulation, and fire protection all meet standards, the project will fail final inspection simply because the bathroom and kitchen plumbing fixtures lack WaterMark certification.

Many Chinese factories promise to "replace with Australian standard fittings" in their quotes, but in practice, pre-installation of plumbing systems involves a series of interconnected issues such as pipe routing, interface specifications, and water pressure design, which cannot be solved by simply "changing a tap."

4.2 CodeMark: Voluntary but Critical "Passage Ticket"

CodeMark is Australia's building product certification scheme (CodeMark Australia Certification Scheme). Although it is voluntary, in practice, it serves as a "passage ticket" for prefabricated buildings entering the Australian market. Possessing a CodeMark certificate for a wall or housing system can exempt it from repetitive reviews of structure, fire protection, and acoustics by local councils, greatly simplifying the approval process.

For prefabricated housing companies, obtaining CodeMark certification means that their product system has undergone a comprehensive evaluation by an independent third party. Certifiers can directly sign off based on the CodeMark certificate without having to individually review every technical detail. This not only reduces project approval uncertainty but also significantly shortens the approval cycle.

However, the process of obtaining CodeMark certification is lengthy and expensive, typically requiring 12-18 months of evaluation and hundreds of thousands of Australian dollars in fees. This represents a significant upfront investment for most Chinese factories, especially when they have not yet secured Australian market orders.

4.3 NATA Steel Traceability: The Root Cause of Structural Engineers' Inability to Sign Off

NATA (National Association of Testing Authorities, Australia) is Australia's national association for testing authorities, responsible for accrediting laboratories and testing bodies. In the construction sector, traceable mill certificates issued by NATA-accredited laboratories are a necessary prerequisite for structural engineers to sign structural adequacy certificates.

Many Chinese factories use Q235/Q345 steel, which is perfectly compliant under Chinese standards. The problem, however, is that these factories cannot provide traceable mill certificates issued by NATA-accredited laboratories, preventing Australian structural engineers from signing structural adequacy certificates. Without a structural engineer's sign-off, certifiers will not issue construction certificates, and the project cannot commence.

The solution to this problem is either to use products from NATA-accredited steel suppliers (typically Australian local or Japanese/Korean steel companies) or to send Chinese steel to a NATA-accredited laboratory for independent testing and obtain traceable reports. Either way, this needs to be planned during the design phase, not as a remedy after product production.

5. Core Design Blind Spots: Why "Australian Design" Must Come First

5.1 Wind Loading: Connection-Dominated Design Logic

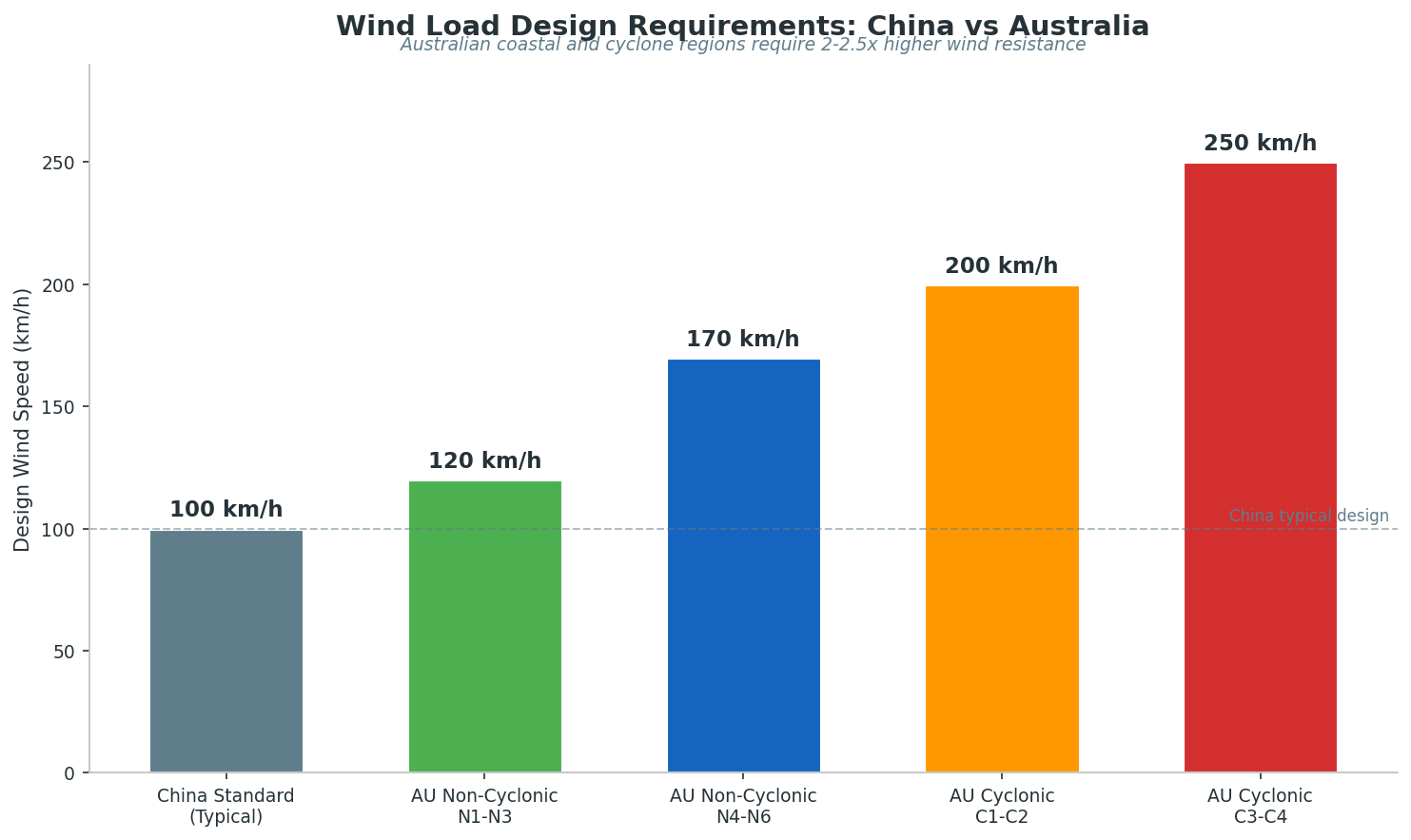

Wind load design is one of the most critical technical blind spots for Chinese prefabricated homes in Australia. Chinese prefabricated components are typically designed according to domestic standards, with a typical wind load of approximately 100km/h. However, Australian wind load requirements are significantly higher—design wind speeds for non-cyclonic regions are 120-170km/h, while coastal and cyclonic regions require even higher speeds of 200-250km/h or more [3].

More importantly, the core logic of Australian wind load design is "connection-dominated". This means that wind resistance depends not only on panel thickness or steel strength but, more critically, on the strength of bolts, welds, and hold-down connectors. Every connection point—wall panel to foundation, roof to wall, and wall panel to wall panel—must be specifically designed and calculated according to AS1170.2 wind load standards.

This difference means that simply transporting Chinese standard prefabricated components to Australia is far from sufficient. Even if the panels themselves are strong enough, if the connection methods do not comply with Australian standards, the entire structure still poses a safety risk in extreme weather. This is why Australian structural engineers are reluctant to sign off on overseas-designed connection details—they cannot confirm whether these connections can withstand Australia's unique wind load conditions.

5.2 7-Star Energy Efficiency Standard (NatHERS): A Mandatory Course Before Factory Order

As of May 2024, Australia mandates that all new residential buildings (including granny flats) achieve a 7-star energy efficiency rating (NatHERS Rating). This is a significant policy change that directly impacts the thermal insulation design of prefabricated home walls, roofs, and floors.

The 50mm EPS (Expanded Polystyrene) sandwich panels commonly used by Chinese factories typically achieve a thermal resistance (R-value) of only R-1.5, whereas NCC 2024+ requires a minimum R-value of R-2.5 or higher. This means that prefabricated homes using standard Chinese sandwich panels fall far short of Australian regulatory requirements for energy efficiency.

The key to solving this problem is that a computer model optimisation must be performed by an Australian registered energy efficiency assessor (NatHERS Assessor) before the factory order is placed. The assessor will calculate the specific insulation solution required to meet the 7-star energy efficiency rating, based on factors such as the project's climate zone, orientation, window area and type, and shading design. This solution must be determined before factory production, as it directly affects core parameters such as wall panel thickness, insulation material selection, and window specifications.

5.3 Deep Design from "Door Panels to Screws"

Based on the above analysis, for prefabricated homes to truly adapt to the Australian market, the systematic design must be led by an experienced local Australian team. This design is not merely drawing a few renderings or simply "translating" mature overseas products; it requires a comprehensive consideration of the entire chain, from planning restrictions, approval logic, structural systems, construction paths, transport limitations, on-site installation conditions, to certifier acceptance.

What determines whether a project can be realised is never just the factory's production capacity, but whether the local team is willing and able to transform it into an Australian product that can be signed off, constructed, and replicated. Who designs it, who bears structural responsibility, who explains the connections, who is responsible for fire protection, waterproofing, moisture resistance, wind resistance, fixing methods, installation processes, and who ensures the certifier is willing to sign off—these questions cannot be avoided.

6. Sydney Granny Flat Market Demand Analysis

6.1 Housing Shortage: Structural Supply-Demand Imbalance

The National Housing Accord, signed by the Australian federal government in 2022, set a target of building 1.2 million new homes within five years from July 2024, meaning 240,000 homes annually. However, actual completions are significantly behind this target.

According to NSW Planning's housing supply forecast data, Greater Sydney is expected to add approximately 28,300 new homes in 2024-25, compared to a peak of 42,000 in 2017-18 [13]. Even under the most optimistic forecast scenarios, Sydney's housing supply cannot meet the demand driven by population growth.

6.2 Immigration-Driven Demand Surge

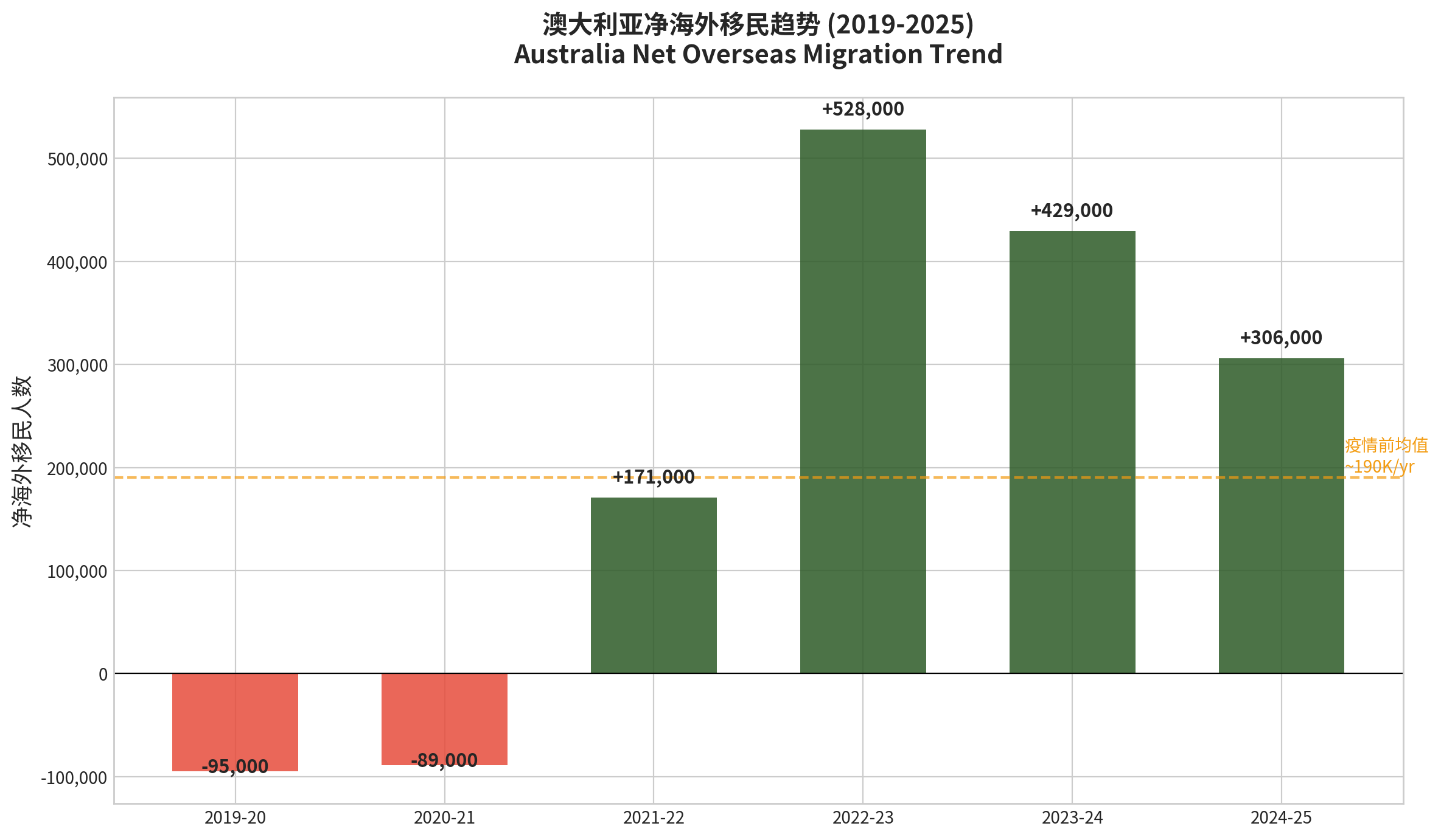

Australia's Net Overseas Migration (NOM) experienced a dramatic rebound after the pandemic. NOM reached a record approximately 528,000 in 2022-23 and about 429,000 in 2023-24, far exceeding the pre-pandemic annual average of approximately 190,000 [14].

This wave of immigration directly translates into immense housing demand. Sydney, for example, as the preferred settlement city for new immigrants, bears the greatest pressure on its housing market. Granny flats, as a "plug-and-play" housing solution—utilising the backyard space of existing properties without requiring new land—have become the most direct means to alleviate this pressure.

6.3 Policy Tailwinds and Market Boom

2026 is a pivotal year for Australia's granny flat market. Several policy reforms are accelerating the boom in this market:

Federal Level: HIA is advocating for a national uniform granny flat framework to eliminate regulatory discrepancies between states [1].

New South Wales: The NSW Parliament is conducting an inquiry into "Rural Housing and Second Dwellings Reform," aiming to further relax restrictions on granny flat construction [15]. NSW currently offers a CDC (Complying Development Certificate - fast approval) pathway for eligible granny flats, with approval in as little as two weeks. This bypasses the lengthy land development cycle of House & Land projects and is currently the only path to achieve "3-4 months from order to occupancy."

Victoria: From March 2026, new planning regulations make it easier for homeowners to rent out small secondary dwellings [16].

New Zealand: For reference, New Zealand legislated in October 2025 to allow the construction of 70-square-metre granny flats without resource consent or building consent [17].

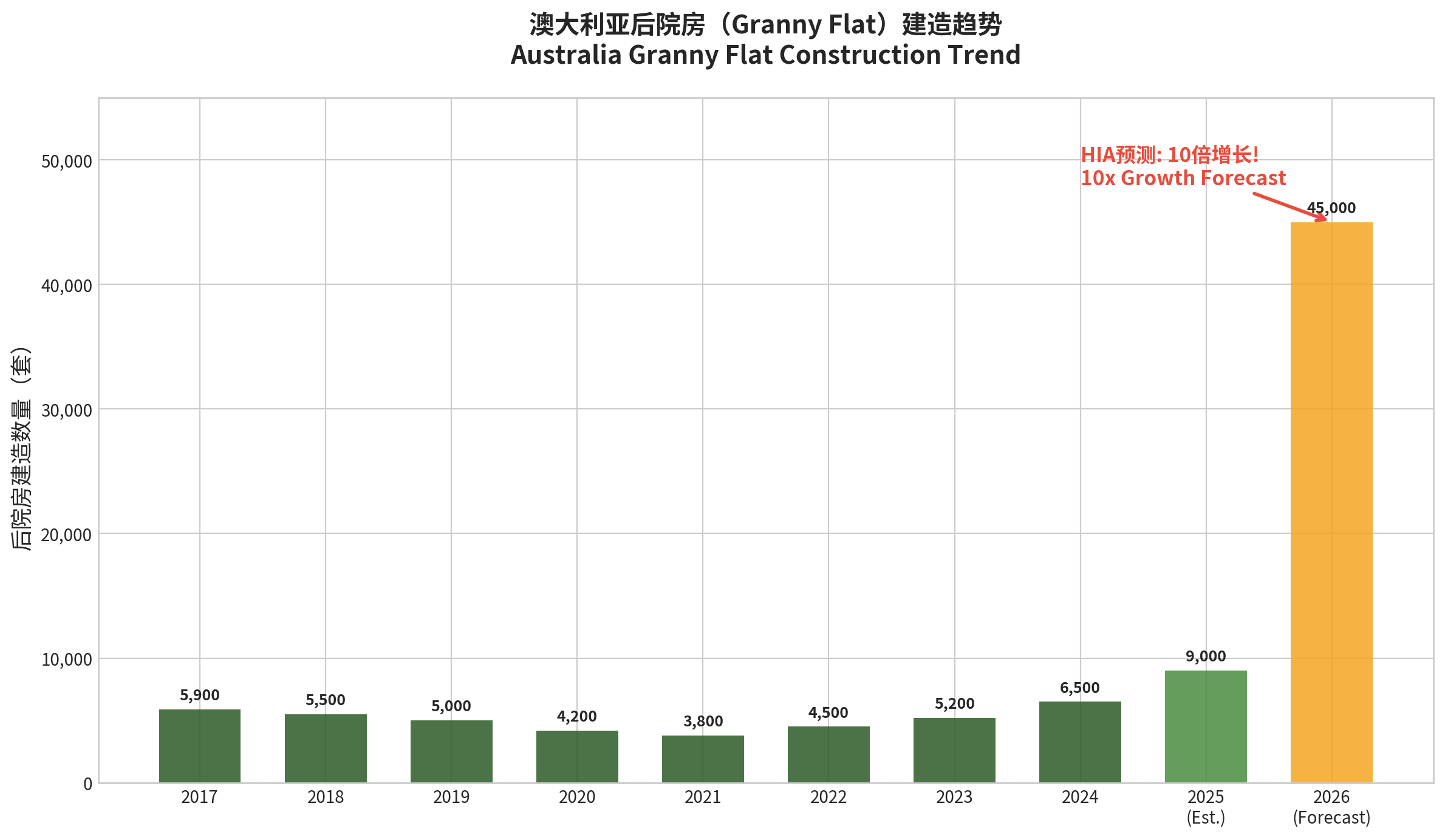

HIA's member survey data is particularly striking:

"Builders expect to construct 10 times the number of granny flats in 2026 compared to 2022." [1]

Based on an estimated 4,500 granny flats in NSW in 2022, a tenfold increase would mean approximately 45,000 granny flats could be built in NSW alone in 2026. While this figure might include national estimates, even discounted, it represents a multi-billion dollar market.

6.4 Rental Yield: Investment Attractiveness

The investment return on granny flats is highly attractive in the current market environment. According to Fundd's 2025 granny flat guide:

"A typical two-bedroom secondary dwelling in Sydney and Melbourne currently generates around $36,000 in annual rental income." [18]

Based on an estimated construction cost of A$170,000 for a prefabricated granny flat, the gross rental yield can reach 21.2%, far exceeding the approximately 3-4% rental yield for Sydney detached houses. Even after accounting for depreciation, maintenance, and management costs, the net return remains very substantial.

| Investment Type | Cost | Annual Rental Income | Gross Yield |

|---|---|---|---|

| Prefabricated Granny Flat (60sqm) | ~$170,000 | ~$36,000 | ~21.2% |

| Traditional Granny Flat (60sqm) | ~$220,000 | ~$36,000 | ~16.4% |

| Sydney Detached House (Median Price) | ~$1,200,000 | ~$42,000 | ~3.5% |

7. Lending Environment and Financing Challenges

7.1 Tightening Lending Criteria

The Australian Prudential Regulation Authority (APRA) has continuously tightened housing lending standards over the past two years. Major banks impose the following restrictions on granny flat projects:

Firstly, most mainstream banks do not include the anticipated rental income from granny flats in the loan applicant's repayment capacity assessment, meaning borrowers must rely entirely on their own income to secure loan approval. Secondly, the valuation of granny flats is often lower than their construction cost, as bank valuers tend to consider them "ancillary structures" rather than independent dwellings. Thirdly, some banks require the loan-to-value ratio (LVR) for granny flat projects not to exceed 80%, which is higher than the 90-95% ceiling for standard home loans.

7.2 Additional Financing Hurdles for Prefabricated Homes: Financial Disconnect

Prefabricated construction faces additional challenges in financing. Traditional construction loans typically use a "progressive payment" model, where banks release funds incrementally upon completion of each construction stage. However, a significant portion of prefabricated construction costs occurs during the factory production stage (especially offshore production), rather than the on-site construction stage, which fundamentally mismatches the banks' traditional disbursement model.

Australian banks currently lack "progress payment" financial products for offshore-produced prefabricated homes. Only when Chinese-funded enterprises or local developers can provide similar trust guarantees or complete the local assembly stage can the purchasing power of ordinary households be unlocked. Furthermore, the attitude of insurance underwriters towards prefabricated construction is changing. The updated NCC 2025 requires clearer traceability, and insurance underwriters are rejecting "ambiguous certifications" [9], which further increases the difficulty of obtaining financing for prefabricated construction projects.

7.3 Exploring Financing Solutions

Despite the challenges, the market is exploring various financing solutions: some non-bank lenders have started offering loan products specifically for granny flats; some prefabricated housing companies provide "Build Now, Pay Later" instalment plans; additionally, utilising refinancing of existing properties to fund granny flat projects is also a common strategy.

8. Granny Flats vs. House & Land Packages: Market Blind Spot Analysis

8.1 A Common Market Confusion

There is a significant cognitive blind spot in the current market: many developers and investors confuse "prefabricated granny flats/secondary dwellings" with "prefabricated construction in new estate House & Land Packages." While both employ prefabricated construction techniques, their market logic, economic models, and target customers are entirely different.

8.2 Granny Flats: Incremental Housing with Zero Land Cost

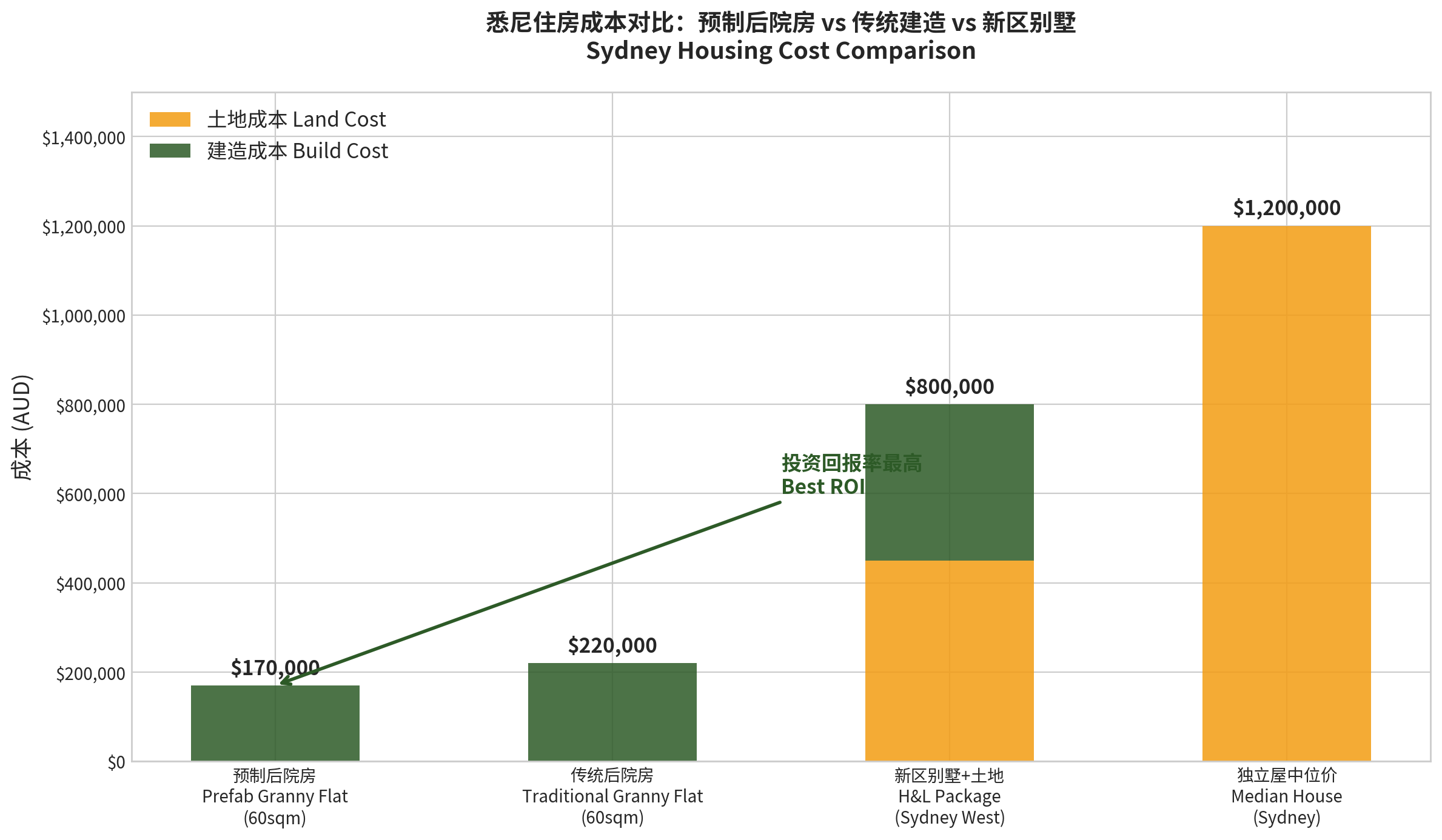

The core economic advantage of granny flats lies in zero land cost. Homeowners utilise the backyard space of their existing property to build a secondary dwelling, without needing to purchase new land. In Sydney, for example, a 60-square-metre prefabricated granny flat costs approximately A$170,000 to build, while a traditionally built granny flat of the same size costs around A$220,000. Prefabricated methods not only save about 23% in construction costs but also shorten the construction period from the traditional 16-24 weeks to 8-12 weeks.

From a market demand perspective, granny flats are not just a story of "low-cost housing alternatives," but a real demand market formed around the re-utilisation of existing land value, changing family structures, increased rental income, and enhanced living flexibility. For many homeowners who already own land, adding an independent dwelling unit in the backyard is essentially, in an era of high land prices, releasing the second value of their land with relatively controllable construction costs.

8.3 House & Land Packages: Land Cost as the Core Bottleneck

In contrast, prefabricated construction in new estate development (House & Land Packages) faces entirely different economic logic. In new development areas in Western Sydney, for example, a block of land suitable for a detached house typically costs over A$400,000-A$500,000, plus A$350,000 in construction costs, bringing the total investment to at least A$800,000. In this cost structure, land cost accounts for 50-60% of the total investment, and the cost savings from prefabricated construction are negligible in the overall investment.

| Comparison Dimension | Prefabricated Granny Flat | Prefabricated New Estate House (H&L Package) |

|---|---|---|

| Land Cost | $0 (utilises existing backyard) | $400,000-$500,000+ |

| Construction Cost | ~$170,000 | ~$350,000 |

| Total Investment | ~$170,000 | ~$800,000+ |

| Prefabricated Savings Ratio (vs. traditional) | ~23% | ~10-15% |

| Annual Rental Income | ~$36,000 | ~$42,000 |

| Gross Yield | ~21.2% | ~5.3% |

| Approval Pathway | CDC (10-20 days) | DA (40-90 days) |

| Target Customer | Existing homeowners (value-add investment) | First-home buyers/developers |

| Market Scale Elasticity | High (existing villa backyards) | Low (limited by new land supply) |

Therefore, the role of prefabricated construction in the H&L Package market is more about "solving construction efficiency issues" rather than "creating new market opportunities." The real market boom lies in granny flats—a niche market almost unrestricted by land supply, with simplified approval processes, and very high investment returns.

9. Sydney Backyard Construction Realities: From "Large Modules" to "Systematic Deconstruction"

9.1 Unique Constraints of Sydney Backyards

Sydney granny flats differ significantly from modular projects on open plots: they are not idealised "blank construction sites" but rather scenarios severely constrained by real-world conditions. Many projects have extremely specific construction conditions—narrow frontages, limited side access (often only 900mm-1200mm wide), sensitive neighbourhood environments, restricted crane radii, controlled on-site access times, and factors such as trees, power lines, fences, and the position of the original dwelling, all of which can directly impact installation methods.

In the past, the market was not short of scattered attempts at prefabricated construction, but many projects ultimately stalled not because of the product itself, but because of the site access stage, especially lifting issues. Once a system relies too heavily on large lifting equipment, it immediately faces very real practical barriers: not every site is suitable for lifting, and not every backyard has the conditions for large cranes to enter, lift, rotate, and operate safely. Many solutions work on paper, but on-site, it becomes clear that installation cannot be completed economically or efficiently.

9.2 Why "Large Modules" Are Not the Optimal Solution

Many overseas companies have been trying to find a shortcut: hoping to enter the Australian market directly with existing models, modules, and production lines. However, a truly mature path often does not start by pursuing "large modules" or "full-box" entry, but rather by beginning with methods that are more aligned with local construction experience.

Prefabrication does not equate to "large modularisation," nor does it equate to "transporting entire buildings." For the numerous backyard scenarios in Australia, especially Sydney, a more reasonable approach is to first disassemble the house into a system of standardised, transportable, and installable components—panels, sections, individual pieces. Through long-term construction practice, validate connections, installation methods, error control, and on-site adaptability, and then gradually evolve to higher-level modular designs.

9.3 Systematic Deconstruction Design: The True Technical Core

Therefore, the prefabricated approach that is truly adapted to local conditions and genuinely suitable for the Sydney backyard market should not merely pursue "the more complete it is in the factory, the better," but should return to the site itself:

First, how can components enter through the side gate—most Sydney detached houses have limited side access width, and component dimensions must adapt to this physical constraint.

Second, how to advance components to the backyard through limited access—components must not only fit through the side gate but also be able to turn in narrow passages and be advanced to the installation location in the backyard.

Third, how to minimise reliance on lifting—reducing or eliminating the need for large cranes can significantly lower construction costs and site requirements.

Fourth, how to achieve rapid assembly without sacrificing construction efficiency—systematic deconstruction design needs to ensure the speed and precision of on-site assembly.

Fifth, how to balance installation precision with on-site operability—the precision advantage of factory prefabrication needs to be maintained during on-site installation.

Based on systematic deconstruction design, calibrated by local construction experience, and constrained by lateral transport and backyard access, ultimately forming a lightweight modular system that possesses both industrial efficiency and is truly suitable for local land conditions.

This point is extremely important. Because the true winners in the future will not be factories with the lowest manufacturing costs alone, but those teams that can integrate design, transport, installation, and approval. Whoever can solve the "last mile from drawing to backyard" truly holds the market entry point.

10. Supply Chain Resilience and Hybrid Production Models

10.1 Fragility of Global Supply Chains

The global geopolitical landscape in 2026 has made supply chain resilience a core concern across all industries. The World Economic Forum (WEF) noted in its March 2026 report that risks to global material supply chains include "concentration of reserves, protectionist trade policies, and geopolitical tensions" [19]. McKinsey Global Institute's 2026 update further analysed how geopolitics is reshaping global trade patterns [20].

As Australia is an island nation, shipping disruptions and biosecurity inspections (e.g., timber must comply with BICON system treatment, 0% asbestos testing) remain high-risk points. Grant Thornton explicitly warned in a client alert in March 2026:

"Geopolitical shocks are reshaping supply chains – what this means for tax, trade, GST and Incoterms controls." [21]

The ongoing escalation of conflicts in the Middle East has had a direct impact on Australian construction costs. Rider Levett Bucknall (RLB) noted in its April 2026 analysis:

"The Middle East conflict is already adding to cost pressures in the Australian construction industry. Higher oil and gas prices are pushing up construction costs." [22]

10.2 "90% Offshore + 10% Local" Hybrid Model

Against this backdrop, the "90% offshore production + 10% local fabrication" hybrid model demonstrates unique supply chain resilience advantages:

Offshore production (90%) covers all prefabricated components that can be completed in a factory environment—including steel structural frames, wall panels, roof panels, window and door assemblies, pre-wired electrical systems, and pre-assembled plumbing. The advantage of factory production lies in controllable quality, independence from weather conditions, and the ability to leverage China's economies of scale and labour cost advantages.

Local fabrication (10%) covers work that must be completed on-site—including foundation pouring (which must be designed according to specific site soil conditions), lifting and connecting prefabricated components, final connection of utilities (water, electricity, gas), and all stages requiring on-site inspection by a certifier.

The core advantage of this model is that it distributes supply chain risks between factory stages that are "batch-producible and storable in advance" and local stages that "must be completed on-site but have limited workload." Even if there are short-term shipping disruptions, existing stock of prefabricated components at port can support several weeks of installation work.

ASCE (American Society of Civil Engineers) research in 2025 also confirmed the advantages of prefabricated construction in terms of supply chain resilience [23].

11. Four Prerequisites for Market Boom and Strategic Recommendations

11.1 Condition One: Full-Process Design Involvement from Australian Local Architectural and Structural Firms

This is the most critical and often overlooked condition. Chinese factories must recognise a fundamental truth: in the Australian market, design authority must reside with locally registered architects and structural engineers. This is not merely "design review" or "stamping," but rather "active design" from the door panel to every screw, which must be undertaken by Australian firms.

Only when local firms are willing to take design responsibility will certifiers sign off; only with certifier sign-off can projects obtain construction permits; only with construction permits will banks release funds; and only with bank funding can the market operate at scale. This is a complete chain of trust, and the absence of any link will cause the entire chain to break.

11.2 Condition Two: Sufficient Market Demand

The scale of market demand determines whether local firms are willing to invest resources in standardising prefabricated home designs. If there are only dozens of orders per year, firms will not develop specialised design systems for this. The good news is that HIA data suggests that 2026 market demand is approaching a tipping point—a tenfold growth expectation implies sufficient order volume to support the investment in standardised design.

11.3 Condition Three: Strong Market Sales Channels

Demand alone is not enough; effective sales channels are also needed to convert demand into orders. This includes: Chinese language marketing channels targeting the Chinese community (given the supply chain advantages of Chinese factories), English digital marketing targeting local homeowners, a network of partnerships with real estate agents and investment advisors, and physical experiences such as display centres and show homes.

11.4 Condition Four: Viable Financing Solutions

In the current environment of continuously tightening lending criteria, innovative financing solutions are the final piece of the puzzle for market growth. This may include: partnering with non-bank lenders to develop specialised granny flat loan products, offering flexible instalment plans, and assisting homeowners in utilising the equity in their existing properties for refinancing.

11.5 Core Conclusion

The Sydney prefabricated granny flat market is on the cusp of a boom. All demand-side conditions—housing shortage, immigration growth, policy tailwinds, rental yields—are mature. The core bottleneck on the supply side is the establishment of a compliant pathway, and the solution to this bottleneck is clear: design led by local Australian architectural and structural firms, with Chinese factories acting as controlled manufacturing segments providing high-quality, low-cost prefabricated components, and local teams completing foundations and installation.

The real market opportunity lies not in new estate development (H&L Packages) but in utilising the backyard space of hundreds of thousands of existing villas in Sydney to add a high-value rental unit to each property through prefabricated granny flats. This model requires no new land, has simplified approval processes (CDC pathway), short construction periods (8-12 weeks), and high investment returns (gross yield over 20%), making it the optimal path to address Australia's housing challenges.

However, this "eve of the boom" is not the eve of factory expansion, nor the eve of promotional hype, but rather the eve of the true maturation of local design systems, construction systems, and standardised product systems. Whoever can achieve this first will not just be selling a granny flat, but will be defining a new way of residential supply for Sydney's next phase.

11.6 Strategic Recommendations

For prefabricated housing companies (e.g., EASOVA):

First, establish and deepen strategic partnerships with Australian local architectural and structural firms to ensure all compliance requirements are met from the design source—including WaterMark plumbing certification, NATA steel traceability, and 7-star energy efficiency modelling. This is the core competitive barrier.

Second, focus on the granny flat market rather than the H&L Package market. The granny flat market has greater growth potential, higher competitive barriers (requiring solutions across the entire chain of design, manufacturing, installation, and compliance), and higher investment returns.

Third, adopt a systematic deconstruction design approach rather than pursuing "large modular complete units." Develop a lightweight modular product system suitable for Sydney backyard scenarios, constrained by lateral transport and backyard access.

Fourth, develop standardised product lines to reduce unit costs through economies of scale. When order volumes reach a certain scale, the design costs for local firms can be significantly amortised.

Fifth, actively participate in the ABCB's National Voluntary Certification Scheme and strive to obtain CodeMark certification, which will create a significant advantage in future market competition.

For investors:

Granny flat investments offer a very high risk-adjusted return in the current market environment. It is recommended to prioritise partnerships with prefabricated housing companies that have mature compliance pathways to ensure projects can smoothly obtain CDC approval and bank financing.

For policymakers:

Accelerating the development of a national uniform granny flat framework and prefabricated building certification scheme, eliminating regulatory discrepancies between states, and reducing compliance costs will help unlock the immense potential of this market and make a substantial contribution to addressing Australia's housing crisis.

References

[1]: HIA & The New Daily. "Bunnings' DIY home embrace sparks national planning push." March 12, 2026. https://www.thenewdaily.com.au/finance/property/2026/03/12/bunnings-granny-flat-planning-shift

[2]: ABS Trade Data & Industry Analysis. Australia prefabricated building import statistics, 2024-25 Financial Year. Total import value A$278.5 million, China share 67.8%.

[3]: ArchiEng. "Why Imported Modular & Prefab Buildings Fail Australian Compliance and How to Fix It in 2026." January 17, 2026. https://www.archieng.au/blog/why-imported-modular-prefab-buildings-fail-australian-compliance-and-how-to-fix-it-in-2026

[4]: Yahoo Finance / Research and Markets. "China Prefabricated Construction Industry Report 2025." February 16, 2026. https://sg.finance.yahoo.com/news/china-prefabricated-construction-industry-report-141800693.html

[5]: Mordor Intelligence. "China Prefabricated Buildings Market Forecasts 2031." January 16, 2026. https://www.mordorintelligence.com/industry-reports/china-prefabricated-buildings-market

[6]: Federal Reserve Bank of Dallas. "China manufacturing overcapacity boosts output, stagnation fears." December 30, 2025. https://www.dallasfed.org/research/economics/2025/1230

[7]: World Steel Association. "World Steel in Figures 2025." 2025. https://worldsteel.org/data/world-steel-in-figures/world-steel-in-figures-2025/

[8]: Dracon NZ. "Australia's Shift Toward Chinese Modular Housing: A Strategic Response to Domestic Challenges." April 4, 2025. https://www.dracon.co.nz/single-post/australia-s-shift-toward-chinese-modular-housing-a-strategic-response-to-domestic-challenges

[9]: Standards Australia. "National Construction Code (NCC) 2025 published." February 17, 2026. https://www.standards.org.au/news/national-construction-code-ncc-2025-published-key-updates-for-australias-building-sector

[10]: NSW Government. "Frequently asked questions for building certifiers." February 5, 2026. https://www.nsw.gov.au/housing-and-construction/compliance-and-regulation/building-certifiers/practice-advice/frequently-asked-questions

[11]: ABCB. "Consultation open: National Voluntary Certification Scheme for Manufacturers of Modern Methods of Construction." July 4, 2025. https://www.abcb.gov.au/news/2025/consultation-open-national-voluntary-certification-scheme-manufacturers-modern-methods-construction

[12]: HIA. "National Voluntary Certification Scheme for Manufacturers of MMC - Issues Paper Submission." August 29, 2025. https://hia.com.au/our-industry/-/media/files/newsroom/submissions/2025/national-voluntary-certification-scheme-for-manufacturers-of-mmc--issues-paper.pdf

[13]: NSW Planning Portal. "Sydney Housing Supply Forecast - Forecast Insights." 2025. https://www.planning.nsw.gov.au/data-and-insights/sydney-housing-supply-forecast/forecast-insights

[14]: Australian Bureau of Statistics. Net Overseas Migration data, various years. https://www.abs.gov.au/

[15]: NSW Parliament. "Rural housing and second dwellings reform - Report No 1." March 2026. https://www.parliament.nsw.gov.au/lcdocs/inquiries/3129/Report%20No%201%20-%20SC%20-%20Rural%20Housing%20-%20FINAL%20VERSION.pdf

[16]: Yahoo Finance Australia. "Aussie landlords seize on granny flat income as council rule change comes into effect." March 24, 2026. https://au.finance.yahoo.com/news/aussie-landlords-seize-on-granny-flat-income-as-council-rule-change-comes-into-effect-032052745.html

[17]: Dan Bidois MP (NZ). "Our Granny Flat bill is now law!" October 22, 2025. https://www.facebook.com/DanBidoisMP/posts/our-granny-flat-bill-is-now-law-from-early-2026-youll-be-able-to-build-a-70sqm-g/1344501817248180/

[18]: Realestate.com.au / Fundd. "Planning reforms unlock $36k rental income from backyard granny flats." December 18, 2025. https://www.realestate.com.au/news/planning-reforms-unlock-36k-rental-income-from-backyard-granny-flats/

[19]: World Economic Forum. "Strengthening global materials supply chains amid new risks." March 2026. https://www.weforum.org/stories/2026/03/materials-supply-chains-collaboration/

[20]: McKinsey Global Institute. "Geopolitics and the geometry of global trade: 2026 update." March 19, 2026. https://www.mckinsey.com/mgi/our-research/geopolitics-and-the-geometry-of-global-trade-2026-update

[21]: Grant Thornton Australia. "Geopolitical instability exposes Australia's supply chain vulnerabilities." March 26, 2026. https://www.grantthornton.com.au/insights/client-alerts/geopolitical-instability-exposes-australias-supply-chain-vulnerabilities/

[22]: Rider Levett Bucknall. "What the Middle East conflict means for Australian construction costs." April 2026. https://www.rlb.com/oceania/insight/what-the-middle-east-conflict-means-for-australian-construction-costs/

[23]: ASCE Library. "Supply Chain Resilience of Prefabricated Construction." January 22, 2025. https://ascelibrary.org/doi/10.1061/JCEMD4.COENG-15514

This report was compiled by Manus AI Research, with data current as of April 7, 2026. Market forecasts in this report are based on public data and reasonable assumptions and do not constitute investment advice.